Concessional contributions to superannuation are pre-tax contributions and can be a great way to save for your retirement as they give you a tax deduction for investing for your yourself – pretty cool!

But did you know that if you haven’t utilised your entire concessional contributions cap limit in previous financial years, you may be eligible to carry forward the unused amounts for up to 5 years?

In this guide, we’ll delve into what carry-forward concessional contributions are, how they work, the pros and cons to consider, and of course how to find out if you have any unused carry forward contribution amounts available to utilise.

Understanding carry-forward concessional contributions

First, let’s break down what concessional contributions are because this is foundational to understanding this strategy.

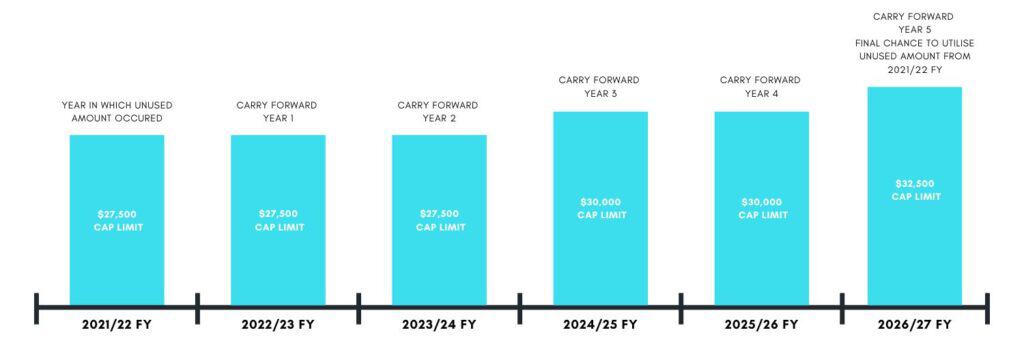

Concessional contributions are contributions made to your super before tax, such as employer contributions, salary sacrifice contributions and personal deductible contributions. In the current 2026/27 financial year, the annual cap for concessional contributions is $32,500.

If you haven’t utilised your full cap limit in previous years, you can carry forward the unused portion for up to five years. For example, in the 2021/22 financial year, the concessional cap limit was $27,500. If you have unused amounts from this year, you have up until the end of this financial year (by 30 June 2027) to utilise them.

This means you can potentially exceed the current years cap limit without penalty.

How to use the unused amounts

In order to utilise the unused carry forward concessional contributions, you first of all have to maximise the current years cap limit. If you then continue to make concessional contributions in excess of the cap, you will start automatically utilising the carry forward contributions available.

If you have multiple financial years with unused amounts, the older cap limits will be used first. In other words, it works on a FIFO basis; First in, first out.

You can utilise multiple years of carry forward amounts in a single year or you can spread it out over multiple future years. In order to work out the best timing, you have to forecast your future tax position, considering when the tax deduction will provide the greatest benefit.

Any method of concessional contribution can be used to utilise the unused amounts, i.e. employer contributions, salary sacrifice, personal deductible contributions or a combination of these.

Of course there are eligibility requirements, so let’s consider this now.

Eligibility requirements

In order to be eligible to utilise the unused carry forward concessional contributions, you need to:

- Be eligible to make a concessional contribution;

- Have unused carry-forward concessional contributions available (we discuss how to find this out soon); and

- Your total super balance must be less than $500,000 at 30 June of the previous financial year.

It is important you assess your eligibility criteria before tying to utilise the carry forward concessional contributions. Failing to do so will result in tax penalties.

Finding your available carry forward concessional contributions

Finding your available carry forward concessional contributions is relatively easy. This can be done through your MyGov account provided you have linked it to the ATO Services.

To find the contributions available, follow these steps:

- Log into your MyGov account;

- Go to ATO linked services;

- In the top banner there is a drop-down box labelled “Super”

- Under the submenu, select “Information” then “Carry-forward concessional contributions”.

This will give you the total of all unused concessional contributions available to carry forward and if you select “Show details” it will break it down by financial year.

Advantages of carry forward concessional contributions

There are many reasons why you might want to utilise your available carry-forward concessional contributions. This can include the following:

- Reduced tax payable: Concessional contributions reduce your assessable income which in turn, reduces the amount of personal income tax you will pay. It can be particularly handy having some carry forward concessional contributions up your sleeve in a year when your assessable income is high due to a bonus, larger than expected business profits, realised capital gain from the sale of an asset, or any other windfall gain that is taxable.

- Boosted retirement savings: By increasing super contributions, you will have more money invested within superannuation for your retirement.

- Tax-efficient savings structure: Superannuation is a tax effective vehicle to save for retirement as earnings within your super fund are taxed at a maximum rate of 15%.

- Forced savings plan: Additional money is allocated to your retirement savings, preventing you from spending it. This creates a great forced savings plan.

Considerations before utilising carry-forward concessional contributions

Despite the many benefits, there are some potential downsides to consider before utilising your available carry-forward concessional contributions. This can include the following:

- Limited access to funds: Superannuation savings are preserved until you meet a condition of release. For most people, this condition is reaching preservation and satisying a condition of release. There are some instances where you may be able to access the benefits earlier such as release on compassionate grounds, financial hardship or under the First Home Buyer Super Saver Scheme.

- Understand your investment strategy and fee structure: Before putting any additional money into superannuation, you want to ensure you understand (and are comfortable with) the investment strategy and fee structure within your super fund.

- Division 293 tax: For high-income earners, if your combined income and concessional contributions exceed $250,000 in a financial year, you may face an additional 15% tax on some or all of your super contributions, totalling a 30% contributions tax.

- Legislative risk: Superannuation is subject to legislative changes meaning rules around superannuation may change which could result in adverse outcomes for you. The further you are away from preservation age, the high the potential risk of legislative changes.

- Exceeding your concessional contributions cap limit: If you exceed your concessional contributions cap limit (including any available carry forward amounts), the excess contribution is included in your assessable income. They are then taxed at your marginal rate, less a 15% tax offset to account for the contributions tax already paid by your super fund.

The Guided Investor Approach

Utilising carry-forward concessional contributions is a great strategy to consider for high income earners that have surplus cash flow and are willing to forgo access to their investment until they meet a superannuation condition of release. This is typically a strategy that we will consider in Phases 2 and up of the Wealth Creation process.